Social Security decisions are often framed as a single question: “When should I start drawing benefits?”

That question matters, but it can also be limiting. The better question is: how does Social Security fit into my overall retirement income strategy, including longevity and survivor considerations?

As April is National Social Security Month, we thought it might be helpful to share a practical framework we’ve developed over the years to help clients making decisions about Social Security. Our goal is to help guide clients who are making this important retirement income decision.

To start with the basics, your Social Security benefi ts are calculated based on your 35 highest-earning years. Cost-of-living adjustments (COLAs) are designed to help benefi ts keep pace with infl ation, but your base benefi ts are a function of your personal wage history and when you start taking them.1

The maximum monthly benefi t for a worker retiring at full retirement age (67) is $4,152 in 2026. If you delay Social Security beyond retirement age, you can receive monthly benefi ts of $5,181 for 2026. You can begin claiming Social Security benefi ts as early as age 62, but monthly payments will be reduced for each month they’re received before you reach full retirement age.2

Step 1: Start With the Decision Drivers, Not the Age

When to take Social Security is a major decision all retirees need to make, and it is one of the most common questions we are asked as financial professionals. It may seem like a straightforward choice, but it’s more complex than it appears since there can be advantages and disadvantages to whatever choice you make.

If you were born in 1957 or earlier, congratulations, you’ve already reached full retirement age. If you were born in 1958 or later, your full retirement age can be anywhere between 66 and 8 months, and 67 for those born in 1960 or later. So, decisions must be made.3 Taking Social Security early reduces your monthly benefits, but you’ll also receive those payments for a longer time. At the same time, delaying payments results in fewer Social Security checks during your lifetime, but each check will be larger.

While the math can be confusing, claiming decisions tend to be better made when they are anchored to a few real drivers, including:

What are your health and longevity expectations?

Mortality is never an easy or comfortable discussion, but it is one consideration when making Social Security decisions. No one knows exactly how long they will live, so be honest about what is likely and how much you want to consider the possibility of a long life. The average life expectancy for a 65-year-old is about 84 years for males and 87 for females, according to the Social Security Administration (SSA). Married individuals tend to live even longer, with an average probability of at least one spouse living to age 90.3

But remember, those ages are just averages. Your personal health status, occupation, and family history may affect how long you live, which may influence your decision on when to start taking benefits.

- Will you continue working?

If you intend to continue working while receiving Social Security, the decision is not only about benefits. It is also about taxes, savings capacity, and how cash flow from other accounts can be sequenced.

If you are still working while collecting Social Security benefits, you may see some of your payments withheld. Even if you are self-employed, earning income can reduce your benefits temporarily. Before your full retirement age, for every $2 you earn above the annual earnings limit of $24,480 in 2026, $1 in Social Security benefits will be deducted. In the year you reach your full retirement age, the reduction falls to $1 in benefits for every $3 you earn above a higher limit of $65,160 in 2026.2

However, the month you hit your full retirement age, your benefits are no longer reduced, no matter how much you earn. The SSA will recalculate your Social Security payments at that time to include the deducted amounts, increasing your benefit.

This article is for informational purposes only and is not a replacement for real-life advice. We can help you better understand how Social Security will affect your overall retirement income, but your tax, legal and accounting professionals can show you how your decision will affect your tax situation. There are many reasons to continue working beyond the obvious monetary ones. If you need the income or just enjoy what you are doing, consider staying on the job. If you are concerned about the cut in benefits, you may want to evaluate postponing Social Security either until you reach your full retirement age or until your earned income is just below the annual limit.3

- What is your household survivor strategy?

A surviving spouse is entitled to benefits based on the deceased spouse’s record. Survivors can typically claim a reduced benefit starting at age 60 (or age 50 if disabled). Benefits will increase the longer the surviving spouse waits, up to 100% of the deceased spouse’s benefit once the surviving spouse reaches full retirement age. Keep in mind that if a deceased spouse took a reduced benefit by claiming early, the maximum benefit of the surviving spouse will also be permanently reduced.2

That makes it important to carefully consider your own benefits, spousal benefits, and survivor benefits when making Social Security decisions that, once made, cannot be changed.

Step 2: Understand the Core Tradeoffs, Early, Full Retirement Age, and 70

While you can choose to begin Social Security payments at any point after you turn 62, there are three main points when benefits change, with a sliding scale in between. Here is what happens at each of these points:1

- Age 62: Benefits are reduced by 30 percent (you receive 70 percent of your full benefit), but you’ll receive payments sooner for longer.

- Age 67 (or a few months sooner if you were born before 1960): Your benefits will be 100 percent.

- Age 70: You reach your maximum “bonus” benefit of 24 percent, but you will receive eight fewer years in payments than if you began benefits right after you turned 62.

If you wait until your full retirement age to start collecting Social Security retirement benefits, you can receive 100 percent of your monthly retirement benefit. However, if you wait even longer than your full retirement age, the Social Security Administration increases your benefit by up to 8 percent for every year you wait (up to age 70).

Here are the maximums for a worker at different ages who earned at or above the taxable maximum over their career.4

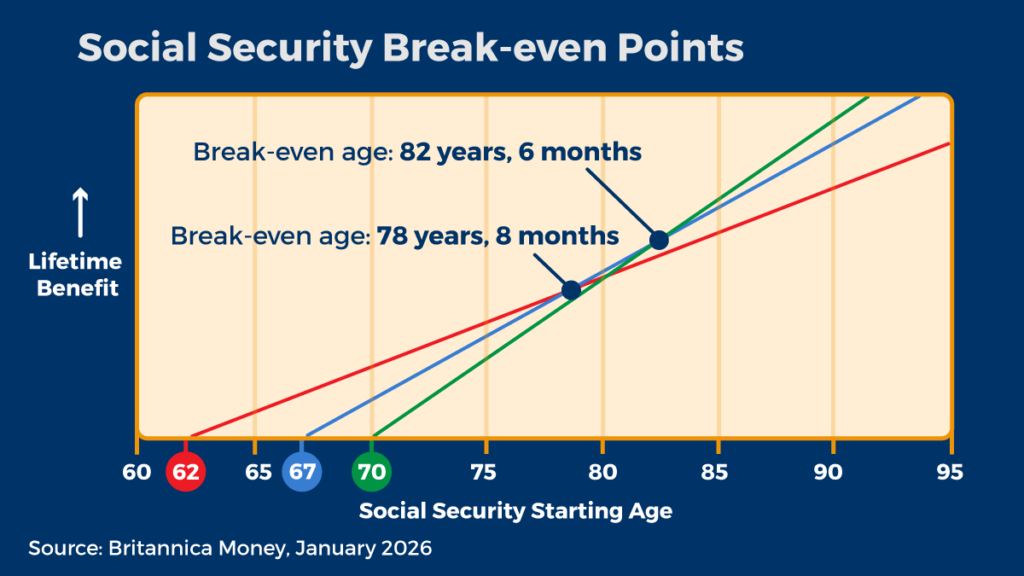

What is Your Break-Even Point?

When deciding whether to take benefits early, you need to consider your break-even point. Your Social Security break-even point is the age at which the total amount you would receive in benefits by claiming early catches up to the total amount you would have received if you’d delayed claiming a few years.

We know that by claiming early, each payment is smaller, but over time, the cumulative amount you receive grows. On the flip side, if you delay benefits, you’ll receive a larger check that will begin to accumulate.

When these two scenarios intersect, that’s your break-even point, when the total benefits received are roughly the same. That typically falls somewhere between ages 78 and 81.5

If you think you will live past 80, waiting to start benefits may make sense. But if you delay payments and don’t live to 80, you are leaving money on the table. That’s why the right framing isn’t simply about the “best age.” It is the “best fit” based on your goals and the trade-off s you are willing to accept.

Step 3: Make Taxes Part of the Decision, Not an Afterthought

Many people are surprised by how Social Security is taxed. The IRS rules depend on something often referred to as provisional income, and up to 50 to 85 percent of benefits may be taxable, depending on income thresholds.6

With the new tax law passed in 2025, Social Security income continues to be taxable, but an additional deduction for seniors may help off set what you have to pay.

Under the One Big Beautiful Bill Act (OBBBA), taxpayers aged 65 or older, and their spouses, if filing jointly, can each claim a $6,000 deduction for tax years 2025–2028. For higher earners, the senior deduction is reduced by 6 percent for adjusted gross income that exceeds $75,000, or $150,000 for joint filers.6

According to White House Council of Economic Advisers’ research, only about 12 percent of seniors will pay taxes on their Social Security benefits due to this new deduction.6 But tax laws can change over time, and this deduction is set to sunset in 2028 if it isn’t extended or made permanent by Congress. So, working with your tax, legal and accounting professionals can help you better understand taxes and your benefits.

While most states do not impose income taxes on Social Security, several still do. Some of these states may allow you to exclude federally taxable Social Security benefits for state income tax purposes based on your adjusted gross income. Review the graph to see where your state falls.6

What is the Forumula Used to Determine Federal Tax on Social Security Income?6

The IRS uses a “combined income formula” to determine if you must pay taxes on your benefits. Combined income includes wages, interest, pension payments, and taxable distributions from retirement plans in addition to nontaxable interest and half of Social Security benefits.

- If you file as an individual and your combined income is:

- Up to $25,000, you pay no tax

- $25,000-$34,000, your benefits may be taxed up to 50 percent

- More than $34,000, your benefits may be taxed up to 85 percent

- Up to $25,000, you pay no tax

- If you file a joint return and your combined income is:

- Up to $32,000, you pay no tax

- $32,000-$44,000, your benefits may be taxed up to 50 percent

- More than $44,000, your benefits may be taxed up to 85 percent

- Up to $32,000, you pay no tax

Are There Additional Social Security Tax Considerations to Keep in Mind?

There are many tax considerations to keep in mind when discussing Social Security. As financial professionals, we collaborate with our clients’ tax professionals to help you better understand your tax situation in the context of your comprehensive financial strategy. Here are a few points to consider:

- The year you claim benefits can create an unexpected taxable event if it coincides with a capital gain or a one-time income event.

- The order of withdrawals within a holistic retirement income strategy matters because withdrawals from different accounts can change how much Social Security becomes taxable due to the combined income levels.

- There may be opportunity windows before taking withdrawals from retirement accounts, where Roth conversions or other moves can be evaluated that may impact Social Security.

Remember, the original Roth IRA owner is not required to take minimum annual withdrawals, so that’s one factor to consider with your overall strategy. Also, with a Roth IRA, to qualify for the tax-free and penalty-free withdrawal of earnings, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances.

We help clients with these and other considerations, not through generic, cookie-cutter answers, but by understanding their unique situations, running scenarios, and presenting options.

Step 4: Consider How Social Security Impacts Your Estate Strategy

Social Security is not inherited in the same way as a retirement or brokerage account. But the claiming decision can still affect legacy outcomes indirectly.

Your level of benefits affects the amount you need to draw down from other accounts to cover living expenses in retirement. This can impact how you position other assets to support your estate strategy or pursue your charitable giving goals.

This can impact your spouse’s cash flow after you are gone. The amount your spouse receives is based on your earnings history, the age you took benefits, and your spouse’s age when you pass.

Your estate strategy may consider a variety of factors beyond just passing on wealth. It should focus on creating a comprehensive financial strategy, and Social Security can be a vital part of that. By considering how Social Security fits into your retirement and post-retirement financial strategies, you may make better decisions about your estate.

Step 5: Use a “Before You File” Checklist

We’ve developed a Social Security Checklist to help our clients who are beginning to evaluate their options.

- Confirm your earning record

SSA compiles a record of earnings that is used to determine benefits. This list is available through your online Social Security account. But errors happen, and it is important to review your historical earnings and correct any issues before claiming.

To check your Social Security statement, visit https://www.ssa.gov/myaccount/statement.html - Review your benefit estimates at multiple claiming ages

SSA makes it easy to use its online tool to review your benefit estimates at different retirement age scenarios. Spending time on the site and playing with the numbers can take the guesswork out of what you would receive and when. - Review your work intentions and the earnings test rules if you are thinking of claiming benefits before full retirement age

If you are looking to claim benefits while still working, you need to be aware of the rules that can temporarily reduce benefits depending on earnings and age. SSA publishes annual earnings limit information as part of COLA updates. - Confirm survivor benefits

You will want to know what will happen when a spouse dies. Questions about what income remains and what changes immediately for the surviving spouse should be discussed and understood before claiming. These considerations may impact when the higher earner decides to take benefits. - Have a tax projection run for the claiming year

Speak with your tax, legal or accounting professional, and see if they can run a tax projection for the year you intend to start your benefits. This can provide some insights that may help you solidify or amend your decision. - Review Medicare premium thresholds and timing

Consider reviewing the Centers for Medicare & Medicaid Services fact sheet for official 2026 figures.

What is the Bottom Line?

The bottom line is that deciding when to begin taking Social Security is a major decision all retirees need to make and one of the most common questions we are asked as financial professionals. It may seem like a straightforward choice, but it’s actually more complex than it seems. There are advantages and disadvantages to whatever choice you make.

Since everyone’s circumstances are unique, there are a few considerations you may want to take into account:

- You may want to consider taking Social Security benefits earlier if:

- You’re no longer working and need the benefits to pay your bills.

- You’re in poor health and don’t expect either you or your spouse to make it to average life expectancy.

- You’re the lower-earning spouse, and your higher-earning spouse can wait to file for a higher benefit.

- You’re no longer working and need the benefits to pay your bills.

- You may want to consider waiting to take Social Security benefits if:

- You’re still working and making enough to impact the taxability of your benefits.

- Either you or your spouse is in good health and expects to live past your average life expectancy.

- You’re the higher-earning spouse, and you’re concerned about the benefits of your surviving spouse.

- You’re still working and making enough to impact the taxability of your benefits.

Don’t Underestimate the Importance of Social Security

If you are approaching your claiming decision, consider treating it like a strategic project, not just a selection on a government form. While Social Security may not be the primary source of retirement income for some, it can still play an important role when developing a comprehensive retirement strategy.

As financial professionals, determining your sources of retirement income and how these different sources can work together is a major part of how we help our clients who are approaching retirement. If you have any questions about retirement income, including Social Security, please do not hesitate to contact our office.

1 Britannica Money, January 2026. https://www.britannica.com/money/social-security-breakeven-calculator

2 NBC Washington, January 14, 2026. https://www.nbcwashington.com/your-money/social-security-benefi ts-changes-2026/4042196/

3 Charles Schwab, March 14, 2025. https://www.schwab.com/learn/story/guide-on-taking-social-security?msockid=37a2e58496ac672b39a4f4af9742667d

4 SSA.gov, January 2025. https://www.ssa.gov/oact/cola/examplemax.html

5 Thrivent, December 19, 2024. https://www.thrivent.com/insights/social-security/social-security-break-even-point-what-it-is-how-to-calculate-yours

6 Fidelity, July 9, 2025. https://www.fi delity.com/learning-center/personal-fi nance/is-social-security-taxed