The final months of the year can sneak up quickly, and with them come deadlines, decisions, and distractions. Before the holiday season takes over your calendar, fall can be a valuable window to revisit your financial strategy and make sure you’re closing out the year with intention.

Whether you’re looking to manage taxes or retirement contributions, or get organized before 2026 begins, now is the time to take action.

We’ve put together a practical list of year-end moves to consider—some time-sensitive, others smart to revisit annually. While this list isn’t exhaustive, it can be a helpful starting point as you think about what needs attention.

Tax-Loss Harvesting

While we often encourage clients to stay focused on long-term investment goals—regardless of short-term market movements—there are times when strategic action might help manage your tax situation. One such opportunity is tax-loss harvesting.

Tax-loss harvesting involves selling an investment that has declined in value and using the realized loss to offset capital gains. In some cases, you might be in a position to replace the investment with a reasonably similar asset. If your losses exceed your gains during the year, you might be able to deduct as much as $3,000 in ordinary income. You can also carry forward any excess losses to offset capital gains and income tax in future years.1

That said, this strategy comes with important rules. To avoid triggering the IRS’s wash sale rule, you must wait at least 30 days before repurchasing a substantially identical security, or the loss could be disallowed.2

Because of these nuances, consider working with a tax, accounting, or legal professional who is familiar with the rules regarding tax-loss harvesting.

Roth IRA Conversions

This time of year is often a good opportunity to evaluate whether a Roth IRA conversion makes sense.

Converting a traditional IRA to a Roth IRA means paying taxes on the amount converted now, but potentially managing taxes on future withdrawals. This can be appealing if you expect to be in a higher tax bracket later in life or want to manage future required minimum distributions (RMDs).3

Keep in mind that the amount converted is treated as taxable income in the year of the conversion, which can lead to a larger-than-expected tax bill. To manage that impact, some individuals opt to convert gradually—rolling over a portion each year—while others wait for a lower-income year to use the strategy.3

The primary benefit of a Roth IRA is that qualified withdrawals—those made after age 59½ and after meeting the five-year holding requirement—are tax-free. Unlike traditional IRAs, the original owner of the Roth IRA isn’t subject to RMDs, which can make them a useful estate management tool.4

If you don’t need the funds to meet current living expenses, the assets can continue growing tax-free and eventually be passed on to heirs. Spouses who inherit Roth IRAs are not required to take distributions (unless the original owner has already started taking RMDs). Other beneficiaries, like non-minor children, will need to follow the ten-year withdrawal rule, but those distributions will be tax-free as long as they follow IRS rules.3

That said, Roth conversions aren’t right for everyone. Timing, tax brackets, and estate goals all matter. Before making any decisions, it’s important to weigh the pros and cons carefully and work with a tax, accounting, or legal professional to understand the tax consequences. A financial professional can help determine if the conversion fits with your overall strategy.4

Year-End Charitable Giving

Charitable contributions can happen any time, but giving tends to spike at year-end. In fact, roughly 30% of all annual giving occurs in December, and nearly 10% happens in just the last three days of the year.5

Cash donations aren’t the only way to give. Appreciated assets, real estate, vehicles, and even securities can also be donated, potentially offering both tax benefits and meaningful impact. Below are a few strategies to consider.

Qualified Charitable Distributions (QCDs) from IRAs

For those aged 70½ or older, donating up to $108,000 in 2025 directly from an IRA through a Qualified Charitable Distribution (QCD) is possible. If married and filing jointly, each spouse can contribute up to $108,000 from their respective IRAs.6

Eligible accounts include:6

• Traditional IRAs

• Rollover IRAs

• Inherited IRAs

• SEP IRAs (inactive only)

• SIMPLE IRAs (inactive only)

• Roth IRAs (under limited circumstances)

Meeting Your RMD with a QCD

For individuals aged 73 or older, QCDs can be used to satisfy Required Minimum Distributions (RMDs). The amount donated via a QCD is not included in your taxable income and won’t appear on your personal tax return.6

Donating Appreciated Securities

If you hold investments that have increased in value, consider donating the securities instead of selling them first. Doing so may help you avoid capital gains tax and potentially qualify for a charitable deduction.7

Donating Depreciated Securities

On the flip side, if you hold investments that have lost value, it might make sense to realize the capital loss before donating. This approach may allow you to use the loss to offset future capital gains.7

Donor-Advised Funds (DAFs)

A Donor-Advised Fund is a 501(c)(3) public charity that allows contributions of cash, securities, or other assets. After funding the account, you can recommend grants to your chosen nonprofits over time.7

For those subject to RMDs, it may be possible to direct distributions to a DAF to help satisfy that requirement.

Some donor-advised funds are considered mutual funds and are sold only by prospectus. The prospectus will provide information on charges, risks, expenses, and investment objectives and should be reviewed carefully before investing. Investment companies can provide a prospectus, or you may prefer to ask your financial professional.

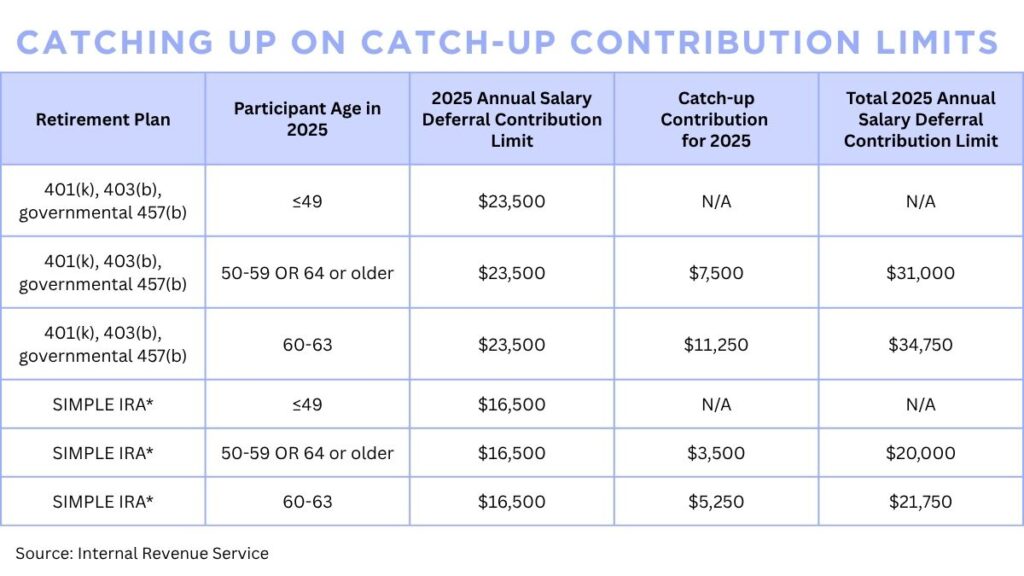

Catch-Up Employer-Sponsored Account Contributions

If you are still working and participating in an employee-sponsored 401(k), 403(b), governmental 457(b), or SIMPLE IRA and are at least age 50 by the end of the year, you can make a catch-up contribution to your account. This is one way to put away more for retirement in these tax-advantaged vehicles. Furthermore, starting in 2025, the Secure Act 2.0 includes a provision that increases the catch-up contribution limit if you turn 60, 61, 62, or 63 (not age 64) by the end of the year.

Refer to the chart below for details on the type of account, age, contribution limits, and catch-up amounts.8

Estate Strategies for Year-End

Year-End Estate Management Considerations

Before gathering with loved ones this holiday season, consider using this time to review your estate strategy. Conversations around personal finances often include estate considerations, and year-end can be a natural moment to revisit these topics.

Below are a few estate ideas to consider adding to your year-end checklist:9

- Account for Major Life Events:

- Reflect on any significant changes in 2025—births, deaths, marriages, divorces, or a move to a different state. Any of these may warrant updates to your estate documents.

- Review Beneficiary Designations:

- Make sure designations for retirement accounts, life insurance policies, and annuities align with your current intentions. Remember, these designations override wills and other legal documents, so consider keeping them current to help manage any confusion.

- Update Key Legal Documents:

- Confirm that your health care proxy and power of attorney forms are in place and reflect your wishes. These documents authorize someone you trust to make medical and financial decisions on your behalf if you’re unable to do so.

- Talk With Your Family:

- Discuss how you’d like to handle personal property—like jewelry, collectibles, or family heirlooms—and share any end-of-life directives. While not always easy, these conversations can help manage confusion or conflict later on. Year-end is often a practical time to have them.

- Use Your Annual Gift Exclusion:

- For 2025, the annual gift tax exclusion is $19,000 per recipient. You can give up to that amount to as many individuals as you wish each year without incurring gift taxes. This strategy may help with your estate management.

529 Contributions

While 529 college savings plans do not have firm contribution deadlines, making contributions before year-end may offer some opportunities. Many families use this time to reassess their financial priorities, and education savings often rise to the top of the list, especially with year-end gifting in view.

Although 529 contributions are not deductible at the federal level, more than 30 states offer a state income tax deduction or credit for contributions, typically only if made by December 31.1 These incentives vary by state but can make a meaningful difference.

Year-end is also a good time to revisit the annual gift tax exclusion, which allows you to contribute up to $19,000 per beneficiary in 2025 without triggering gift taxes. And for those looking to accelerate contributions, the IRS allows “superfunding,” where you front-load up to five years’ worth of gifts—or $95,000 per beneficiary (or **$190,000 for married couples electing to split gifts).2

Not surprisingly, many 529 plans experience a spike in contributions during the winter holidays. Increasingly, parents and grandparents are opting for gift contributions, viewing education savings as a more meaningful alternative to traditional presents. In response, many 529s have rolled out tools that make gifting easier, such as personalized URLs or electronic contribution options for friends and family.10

Making Your Year-End Assessment

As we move into the final quarter of the year, it’s a smart time to step back, review your progress, and make any adjustments that can strengthen your financial position going into 2026.

At our firm, we’re focused on helping clients make informed, proactive decisions, especially when year-end strategies can create meaningful tax and personal finance opportunities. If you’re not currently working with a financial professional, we’d be glad to provide a personalized assessment and share how we’re positioning clients for the year ahead and beyond.

If you have questions about anything we covered or want to talk through your own priorities, please don’t hesitate to reach out.

Before We Go

We discussed many concepts and ideas, so we wanted to take a moment to explain the rules and restrictions for certain types of accounts. Remember, this article is for informational purposes only and is not a replacement for real-life advice. Consult your tax, legal, and accounting professionals before modifying your tax strategy.

Once you reach age 73, you must begin taking RMDs from a traditional IRA in most circumstances. Withdrawals from traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

Similarly, once you reach age 73, you must begin taking required minimum distributions from a SEP-IRA, Simple IRA, and other defined contribution plans. Withdrawals are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

In most circumstances, you must begin taking required minimum distributions from your 401(k) or other defined contribution plan in the year you turn 73. Withdrawals from your 401(k) are taxed as ordinary income, and if taken before age 59½, may be subject to a 10% federal income tax penalty.

To qualify for tax-free and penalty-free earnings withdrawals, Roth IRA distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawals can also be taken under certain other circumstances, such as the owner’s death. The original Roth IRA owner is not required to take minimum annual withdrawals.

The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities have contract limitations, fees, and charges, including account and administrative fees, underlying investment management fees, mortality and expense fees, and charges for optional benefits. Most annuities have surrender fees that are usually highest if you take out the money in the initial years of the annuity contract. Withdrawals and income payments are taxed as ordinary income. If a withdrawal is made prior to age 59½, a 10% federal income tax penalty may apply (unless an exception applies).

Several factors affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder may also pay surrender charges and face income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

A 529 plan is a tax-advantaged college savings plan. Before choosing a plan, it’s important to consider not only the state tax treatment but also any associated fees and expenses. Availability of a state tax deduction will depend on your state of residence, as state tax laws and treatment may vary from federal tax laws. If you make nonqualified distributions, earnings will be subject to income tax and a 10% federal penalty tax.

Sources

1 Fidelity, March 26, 2025

https://www.fidelity.com/viewpoints/personal-finance/tax-loss-harvesting

2 Fidelity, May 30, 2025

https://www.fidelity.com/learning-center/personal-finance/wash-sales-rules-tax

3 Investopedia, November 10, 2024

https://www.investopedia.com/terms/i/iraconversion.asp

4 Investopedia, March 30, 2025

https://www.investopedia.com/ask/answers/05/waitingperiodroth.asp

5 Non-Profits Source, 2025

https://nonprofitssource.com/online-giving-statistics/

6 Fidelity, June 2025

https://www.fidelity.com/retirement-ira/required-minimum-distributions-qcds

7 Nasdaq, March 4, 2024

https://www.nasdaq.com/articles/six-charitable-giving-strategies-for-2024

8 Lord Abbett, June 2025

9 Charles Schwab, June 2025

https://www.schwab.com/resource/estate-plan-checklist?msockid=37a2e58496ac672b39a4f4af9742667d

10 Savingforcollege.com, May 9, 2025

https://www.savingforcollege.com/article/529-plan-contribution-deadlines